On 10 April 2026, the Australian Government released exposure draft legislation to change the way that CGT rules apply to foreign investment in Australian land and natural resources. Notably , the rules include retrospective changes which may mean that completed transactions which are not subject to tax under current rules may become taxable under the new rules (subject to limitation periods not having expired).

Broadly, the proposed changes are to:

- clarify and broaden the types of assets the Australian CGT regime captures for foreign residents to include assets that have a close economic connection with Australian land and / or natural resources;

- increase the number of transactions caught by the CGT regime based on market valuations across a 365-day period;

- increase the ATO's knowledge of high-value transactions; and

- grant a one-off 50% CGT discount for foreign investors who dispose of eligible renewable energy assets in a certain time period.

The Australian Treasury accepted submissions regarding the draft legislation until 24 April 2026.

What is the impact for foreign investors?

This is a very significant reform package for all current and prior foreign investors in Australian real property and mining, water and renewable energy assets. The changes are likely to have a dampening effect on investment decisions, asset valuations and financial returns. Careful tax structuring will be required for all future investments and sales.

Foreign investors should carefully consider whether previously non-taxable transactions could now be taxable. Some measures apply on a prospective basis only with others applying on a retrospective basis. The prospective changes begin on the first 1 January, 1 April, 1 July or 1 October after Royal Assent.

Some of the changes concerning the meaning of 'real property' apply retrospectively from 12 December 2006 (while other changes to that definition apply only prospectively, and not retrospectively). Specifically, in terms of retrospective taxation, the Australian Government is asserting that, since 12 December 2006, it has always intended to tax:

- any interest in or right over Australian land regardless of treatment under any State or Territory law (eg any severance or deeming rules); and

- a thing (or a lease of that thing) that is fixed on Australian land and is expected to be situated on the land for the majority of its useful life (whether or not it is a fixture, or treated in some other way by State, Territory or general law).

Retrospective taxation in respect of the above would only be possible if the review periods for the relevant taxpayers have not expired. The review period is generally 4 years from the date that a tax assessment is issued. This is especially relevant to foreign investors whose prior capital gains or losses have been disregarded, but who have not filed an Australian tax return and not received a tax assessment. This could open up the possibility of the ATO assessing the foreign investor retrospectively under the new rules, due to the review period having not commenced.

With regard to the retrospectivity, on 21 April 2026, the Commissioner released guidance that, in broad terms, confirms he will practically only continue the current compliance approach for disposals that:

- are currently subject to review; or

- have occurred in the past 4 years (being the general period of review).

With regard to managed investment trusts (MIT):

- There is no change to the definition of eligible investment business (EIB) (which is used to assess MIT and public trading trust status). This will mean that an investment in land primarily or solely for the purpose of deriving rent will still need to be assessed by reference to general law concepts. The new rules will further entrench the difference in tax outcomes for foreign investors who invest in eligible Australian land assets for MIT purposes (generally a final 15% withholding tax rate) versus foreign investors who invest in non-MIT structures holding CGT real property (minimum 30% tax rate).

- The new rules could result in historical MIT fund payments being greater than previously calculated, leading to an under-withholding which could subject the trustee and unitholders to review (as no limitation period applies to withholding taxes).

There will be no grandfathering of existing rules for disposals of assets that were acquired before the commencement of the new rules. However, a consolation is that foreign investors who are contemplating a sale may be able to manage the timing of their transaction so that it qualifies for the proposed renewables 50% CGT discount.

What are the key proposed changes?

Capturing more assets in the CGT net: The CGT regime will be expanded to capture assets with a close economic connection to Australian land or natural resources. This will be achieved by expanding both the definitions of real property and taxable Australian real property to include:

- any interest in or right over land;

- a personal right to call for or be granted any interest in or right over land;

- a licence or contractual right exercisable over or in relation to, land;

- assets, and combinations of assets, that are expected to be fixed or installed on land for the majority of their useful life, such as utilities infrastructure, transmission lines, substations, wind turbines and solar panels, large-scale battery energy storage systems and heavy machinery, even if they are removable (e.g. solar panels);

- a lease of a thing, or a licence or contractual right exercisable over, an asset in (d);

- water entitlements to an Australian water resource; and

- an option or right to acquire a CGT asset covered by any of the above.

These assets are in addition to those already caught by the CGT regime. Existing captured assets include freehold land and leaseholds, mining, quarrying or prospecting rights and options or rights to acquire any of these.

We outline our observations below:

Access rights and licences

Real property will now include contractual licences that derive their value from, or in connection with, assets fixed / installed on land that now constitute real property. The explanatory memorandum gives the example of a licence agreement between a data centre operator and a landowner. The data centre operator's rights to access the building on the land in which it houses its servers will now be real property.

Tangible assets

The inclusion of a combination of assets means that assets which are attached to each other are all considered to be fixed or installed on the land, provided that any one of the items is so fixed or installed. As a result, a wider range of disposals by foreign investors may now be subject to Australian tax.

The Government proposes to apply CGT retrospectively to 12 December 2006 in respect of assets that have been treated as excluded from CGT on the basis of State or Territory severance laws or on the basis that they were things fixed to land in Australia and were reasonably expected to be situated on the land for the majority of the thing's useful life (irrespective of whether or not the thing is a fixture or treated in another way under State or Territory law or general law). The date of 12 December 2006 is the date that the current foreign resident CGT regime was introduced. As a result, the ATO could potentially use the new rules to assess historical disposals that a foreign investor previously treated as CGT-free. These changes would overrule the Federal Court's determination regarding the meaning of real property in two recent cases, which have been unfavourable to the ATO, being YTL Power Investments Limited v Commissioner of Taxation [2025] FCA 1317 and Newmont Canada FN Holdings ULC v Commissioner of Taxation (No 2) [2025] FCA 1356. In practice, the enforcement of retrospective taxation may be limited as, on 21 April 2026, the Commissioner released guidance that, in broad terms, confirms he will practically only continue the current compliance approach for disposals that are currently subject to review or have occurred in the past 4 years (being the general period of review).

Market valuation of real property

Some practical valuation questions arise, for example, where value is not attributable to the underlying rights themselves, but to output or broader enterprise value generated from them. It is arguable that, in applying the principal asset test, the market valuation should not take into account the value of an offtake arrangement or goodwill (being a quality or attribute that derives, among other things, from using or applying other assets of a business and is an indivisible item of property that is legally distinct from the sources from which it emanates).

Importation of real property definition

The newly defined real property has been imported throughout the Tax Acts, for example in the:

- Division 230 taxation of financial arrangement (TOFA) rules; and

- Division 250 rules that apply to the tax depreciation of assets used in 'tax-preferred' arrangements involving government, charity or foreign resident end users.

Further analysis will be required to determine whether the broadening of the term will have any practical effect on the operation of these provisions (noting that the explanatory memorandum states "it is not intended or anticipated" to have such an effect).

The new definition of real property will also apply to Australia's double tax agreements, as a result of a proposed amendment to the International Tax Agreements Act, although it appears that it will only apply to double tax agreements prospectively, rather than retrospectively.

Renewables 50% CGT discount

To soften the impact of the changes, after industry consultation, the Government will introduce a temporary 50% CGT discount for foreign residents (including companies and trusts, but not individuals) who enter into contracts to dispose of Australian renewable energy assets (or eligible indirect interests in these assets) between the commencement of the concession (which will be the first 1 January, 1 April, 1 July or 1 October after Royal Assent) up to 30 June 2030. More detail on this further below.

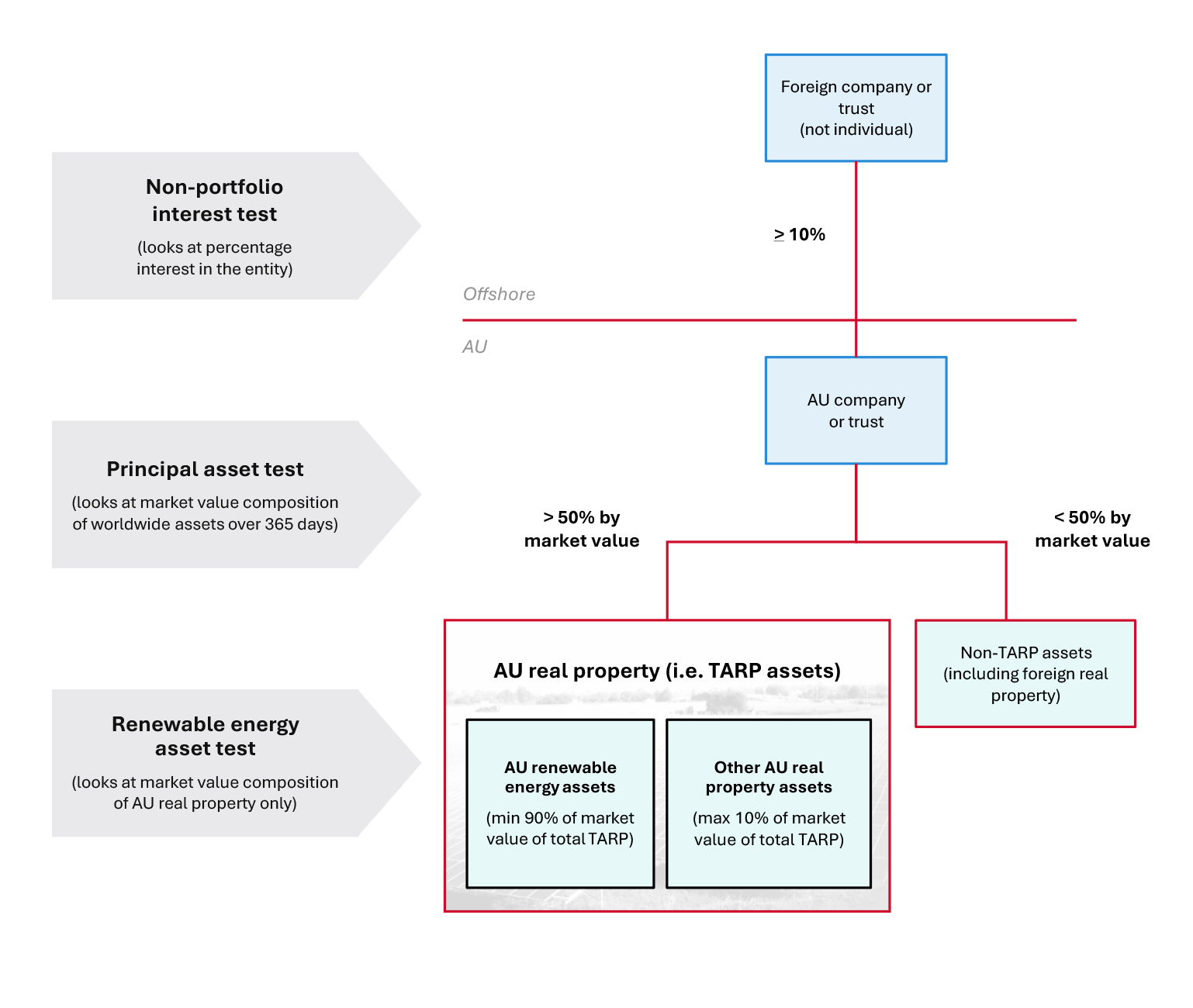

Market value testing period (principal asset test)

For foreign investors who hold shares or units in an entity that holds taxable Australian real property, a new 'look back' 365 day testing period will replace the point-in-time test that currently applies immediately prior to a sale / transfer for assessing whether 50% or more of the market value of an underlying entity's total assets (directly or indirectly held) is derived from taxable Australian real property.

The market value of mining, quarrying or prospecting information relating to an area in Australia will also now be notionally treated as taxable Australian real property for the purpose of applying the principal asset test (although such information is not itself included in the expanded real property definition).

This 'look back' proposed change will remove the ability of a foreign investor to minimise CGT by way of changing the underlying asset composition just before a sale. The new rule will theoretically require a value of the underlying property for every day in the 365-day period, which would be difficult to assess retrospectively, though we expect in practice that valuations may be obtainable for date ranges, particularly for stabilised assets. It may prove more difficult, for example, for mining companies whose valuation is dependent on movements in mineral prices. The 365-day period aligns with the OECD approach, which is reflected, for example, in the Australia-New Zealand tax treaty (as amended by the multilateral instrument). Article 13(4) of that treaty provides that income, profits or gains derived by a resident of a Contracting State from the alienation of any shares or comparable interests deriving more than 50% of their value directly or indirectly from real property situated in the other Contracting State may be taxed in that other Contracting State, if the relevant value threshold is met at any time during the 365 days preceding the alienation.

Furthermore, notwithstanding comments in the explanatory memorandum, complex interactions may apply under a double tax agreement (as amended by any multilateral instrument) where the principal asset test is not satisfied on the particular date the CGT event occurs.

ATO pre-notification requirement

Foreign investors disposing of shares or units worth A$50 million or more (including under split transactions) must notify the ATO within a certain period. Failure to do so will require the purchaser to pay an amount (contractually this is usually treated as a withholding from the purchase price) to the ATO equal to 15% of the purchase price under the foreign resident capital gain withholding (FRCGW) rules. The notification periods are as follows:

| Days between entering the sale contract and settlement |

Notification period |

| Up to 30 days |

As soon as reasonably practicable after entering the sale contract (and definitely before settlement) |

| 31 days or more |

At least 28 days before settlement |

As a failure to notify the ATO will result in the 15% payment obligation, purchasers will now need to see evidence of the notification to the ATO.

Purchaser onus for checking vendor declarations

If a foreign resident vendor declares that the sale shares or units are not subject to CGT, purchasers will be required to withhold an amount from the purchase price under the FRCGW rules if objectively the purchaser could reasonably conclude that the declaration is false. This will place a significantly higher burden on purchasers to undertake considerable due diligence and review information, for example to verify that the vendor is an Australian resident, has not passed the principal asset test (as described above) or the non-portfolio interest test (i.e. the vendor has held at least a 10% direct or indirect interest in the unit trust or company at the time of disposal or throughout a 12 month period that began 2 years before the disposal). This may have significant implications for transaction timetables.

What is the 50% CGT discount for renewable energy assets?

A 50% CGT discount will be available for foreign residents who enter into contracts to dispose of eligible Australian renewable energy assets. It also applies to indirect interests in such assets held on capital account. The concession runs from commencement (the first 1 January, 1 April, 1 July or 1 October after Royal Assent) to 30 June 2030 (i.e. the CGT event, usually entry into the sale contract, must occur after this date and before 30 June 2030). The concession is not available for transactions which occur prior to commencement, or have already occurred, notwithstanding that the changes to the definition of real property will apply retrospectively to those transactions. This may lead to a 'pause' in the market for renewables transactions until commencement.

The discount is available only to foreign residents that are not individuals (e.g. companies and corporate trustees). The discount will not flow through a trust to benefit unitholders / beneficiaries of the trust that are foreign resident individuals.

This is a targeted, one-off concession that is intended to provide transitional relief (noting that foreign residents are not ordinarily entitled to a CGT discount regardless of their entity type).

The two types of eligible assets:

1. Australian renewable energy asset (directly held)

- Taxable Australian real property assets that have the primary purpose of generating, or directly facilitating the generation of, electricity in Australia using an eligible renewable energy source (within the meaning of the Renewable Energy (Electricity) Act 2000 (Cth)), where the generation occurs presently or is to occur in the future.

- An example is grid firming battery energy storage systems (and the underlying land), but not general electricity transmission infrastructure (i.e. poles and wires).

Notes:

- The definition requires the asset to be used for renewable energy generation more than any other purpose for which the asset is used. This suggests that at least 50% of the asset's use must be for renewable energy generation, but it is unclear how this is measured (e.g. by reference to time, financial return or land area).

- The definition covers temporarily dormant assets.

- Prima facie, assets that are only partly or not yet constructed (e.g. land with a development approval) will not satisfy the requirement, unless the surrounding circumstances sufficiently and objectively demonstrate the assets are intended to be used only for renewable energy generation having regard to the land identified for the project, grid connection agreements, development approvals, or rights to future income under an offtake agreement.

2. Eligible membership interests that satisfy the renewable energy asset test

Membership interests (eg shares or units) in an entity where, on a look-through basis, at least 90% of the underlying market value of the entity’s Australian real property assets is attributable to Australian renewable energy assets. This is depicted below (see diagram). The market valuation approach must be the same as that used for the principal asset test. An integrity rule will apply to prevent artificial inflation of values.

Now is the time to review existing and pipeline transactions against these proposed changes and assess whether historical disposals could also be caught.