- The majority of takeover bids are 'hostile', that is, not recommended by the Target Board on first announcement of the bid.

- The success rate for hostile takeover bids is materially lower than for 'friendly' takeover bids, i.e., bids that are recommended by the Target Board on announcement.

- The Target Board's recommendation, and the Bidder's willingness to increase its price to secure that recommendation, are the two major determinants for success of an off-market takeover bid.

- But even with the Target Board's recommendation, a hostile Bidder faces a material risk that it will fail in achieving control of Target.

What is a hostile takeover bid?

A takeover bid can be characterised as either 'hostile' or 'friendly', depending on whether the Bidder has the recommendation of the Target Board that target shareholders should accept the bid.

The precise definition of what is a 'hostile' takeover bid varies – it could include any takeover bid that was not recommended by the Target Board on first announcement of the bid. This includes those 'unsolicited' takeover bids which come as a surprise to the Target Board, but are then recommended soon after first announcement of the bid.

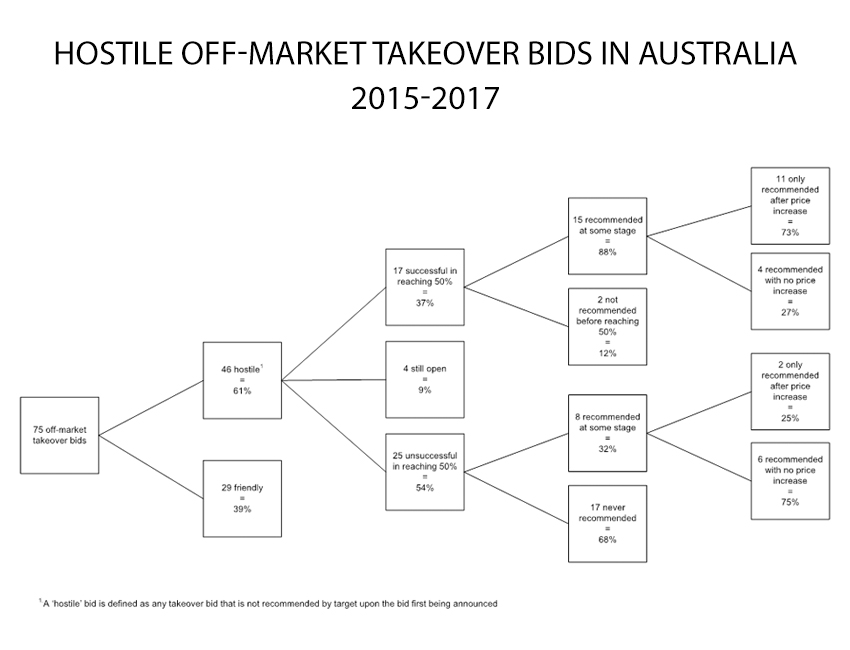

Using that definition, there were 46 hostile off-market takeover bids (of any value) for Australian ASX listed Targets announced between January 2015 and December 2017 . This accounted for 61% of all off-market takeover bids for Australian ASX listed Targets in that period. So, the majority of off-market takeover bids were not recommended by the Target Board on first announcement of the bid.

How successful are hostile takeover bids?

What is interesting about those hostile off-market takeover bids is the likelihood that the Bidder will succeed in achieving control of Target, that is, Bidder reaching ownership of 50.1% or more of Target shares.

Of the 46 hostile off-market takeover bids for Australian ASX listed Target companies announced between January 2015 and December 2017, the Bidder was only successful in achieving control of the Target 17 times . That is, only 37% of all hostile off-market takeover bids during that period succeeded.

This relatively low level of success for hostile bids compares to the 29 friendly off-market takeover bids for Australian ASX listed Target companies announced between January 2015 and December 2017. In those friendly bids, the Bidder was successful in achieving control of the Target 24 times (or 83%).

What makes hostile takeover bids succeed?

Three key factors are most likely to influence whether a hostile off-market takeover bid will succeed:

- The Target Board's initial and final recommendation.

- Whether the Bidder increases its offer price.

- Whether Target's major shareholders are willing to accept the offer, regardless of recommendation.

Target Board recommendation

Recent history shows that the most important factor is whether the Target Board recommends the hostile bid at some stage after it is first announced, even if the Target Board's initial recommendation is to reject the bid.

Of the 17 successful hostile off-market takeover bids between January 2015 and December 2017, the Target Board recommended acceptance of the bid at some stage in 15 cases (or 88%). In one other hostile off-market takeover bid in which the Bidder succeeded in achieving control, the Target Board recommended acceptance, but only after the Bidder had succeeded in reaching 65% acceptances.

Interestingly, in both of the two successful hostile off-market takeover bids that were not recommended, neither Bidder achieved 100% ownership of Target. Both bids stalled below 90%, meaning that the Bidder was not able to rely on compulsory acquisition to reach 100%. This means that there has not been a single example in the last three years of a hostile Bidder reaching 100% without a positive Target Board recommendation at some stage.

Price increases

The other important factor is price, and namely whether the Bidder is prepared to increase its initial bid price to secure a favourable recommendation of the Target Board.

Of the 15 successful hostile off-market takeover bids between January 2015 and December 2017 that were at some stage recommended, the Target Board recommended acceptance of the bid only after the Bidder increased the offer price in 11 cases (or 73%). Only four bids obtained a favourable recommendation without any price rise.

The risk of failure is still material, even with a recommendation

This suggests that hostile Bidders should highly value the Target Board's recommendation, and should be prepared to increase its offer price in order to secure it. However, that strategy alone is not a guarantee of success.

Of the 25 unsuccessful hostile off-market takeover bids between January 2015 and December 2017, the Target Board recommended acceptance of the bid at some stage in eight cases (or 32%). Two of those eight cases included an increase in the offer price by the bidder. So, even where a hostile Bidder secures the Target Board's recommendation, there is a material possibility that the Bidder will still fail in achieving control of the Target.

The impact of major shareholders

The other determinant of success of hostile off-market takeover bids is acceptances by major shareholders.

This factor is less pronounced, as many Targets do not necessarily have one or more major shareholders on their register. But it is plain to see that a holder of 10% or more of Target shares can materially influence the prospects of success for a Bidder aiming to reach 50.1%.

Where major shareholders accept the hostile takeover bid, the bidder can still succeed even where the Target Board recommends against acceptance. We saw this occur in the one successful hostile takeover bid that was never recommended by the Target Board. In that bid, the Bidder achieved success because all of the major shareholders of Target accepted the bid. The acceptances by the major shareholders not only achieved control for the Bidder, but were then used as a key marketing message by the Bidder to encourage other smaller shareholders to accept the takeover bid.

Indeed, where shareholders accounting for a large proportion of the Target's shares accept a hostile bid, it becomes very difficult for the Target Board to maintain a reject recommendation. We saw this occur in Downer EDI's hostile off-market takeover bid for Spotless, where the Spotless Board maintained its reject recommendation until Dower EDI had achieved acceptances of over 65%.

In comparison, where major shareholders do not accept the hostile takeover bid, the bidder faces a material challenge in succeeding. We saw this occur in the hostile off-market takeover bid for Macmahon Holdings Limited by CIMIC Group. In that bid, a major shareholder's refusal to accept was a key reason CIMIC failed to reach control. There, CIMIC held a pre-bid stake in Macmahon of 20.54% and CIMIC's bid quickly reached 23%. One major shareholder in Macmahon held a 5.9% stake – had that stake been accepted into CIMIC's bid, CIMIC would have likely gained substantial momentum and potentially moved closer to 40% quickly. However, the holder of that 5.9% stake sold the entire stake off-market to shareholders who were critical of CIMIC's bid. Without that stake being accepted into CIMIC's bid, the bid stalled at 23%.

A key issue relevant to obtaining acceptances from major shareholders is whether the bid remains conditional, including subject to any minimum acceptance condition (typically 90% or 50.1%). Institutional investors will often not accept a bid while it remains conditional, so Bidders generally need to make a strategic decision at some point during the offer period to waive the conditions in order to obtain acceptances. However, waiving conditions leaves the bidder exposed to concluding the offer without obtaining control of Target, despite having paid a control premium.

Conclusion

Overall, the statistics are somewhat sobering for potential hostile Bidders. There are relatively low chances that a hostile off-market takeover bid will succeed, and even with a positive recommendation of the Target Board, the Bidder still has a material risk of failing to achieve control of Target. This reality gives an indication as to why Bidders should be open to approaching Target to try and reach an agreement on the terms of the Bidder's offer, and the Target Board's recommendation, before the bid is announced.